Key Takeaways

- Asset protection in divorce must be lawful, transparent and supported by clear financial records.

- Property settlements can include assets in one person’s name, jointly owned property, superannuation, businesses, trusts, inheritances and debts.

- Moving, hiding or selling assets without advice can increase legal risk and may affect the final outcome.

- Financial agreements, interim orders and consent orders may help protect your position when used correctly.

- Early legal advice is especially important if you have complex assets, a business, a trust or concerns about urgent financial risk.

Protecting assets during divorce in Australia

Protecting assets means taking lawful steps to protect your financial position during divorce or separation. Under the Family Law Act 1975, the Federal Circuit and Family Court of Australia considers each person’s contributions, future needs, and what is fair. Assets are not automatically divided 50/50, and trusts, businesses, inheritances and jointly owned property may still be counted.

Key things to understand:

- You must be open, honest and supported by clear financial records.

- Trusts, businesses, inheritances and jointly owned property may still form part of the asset pool.

- Early legal advice from a divorce lawyer can help you understand your rights before major decisions are made.

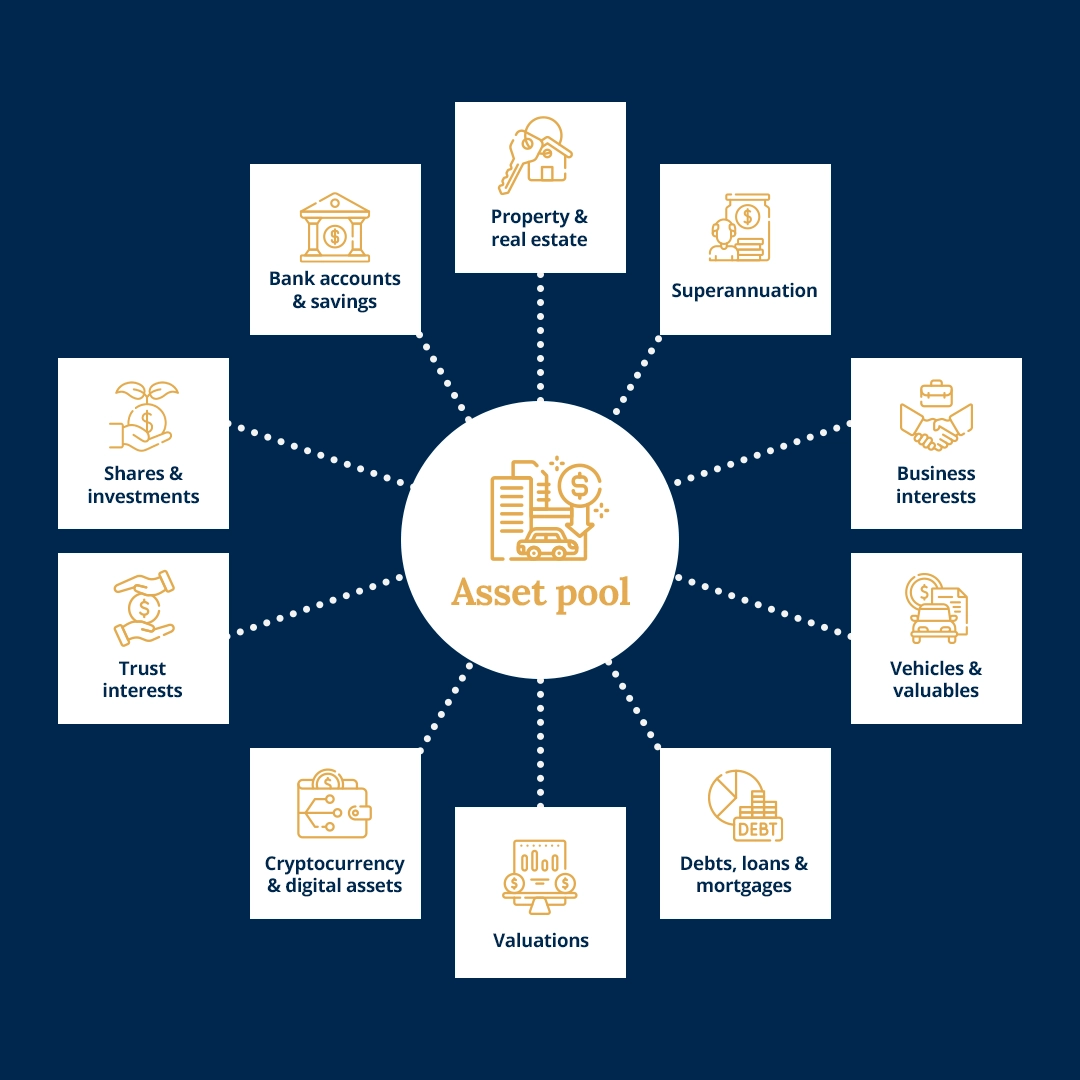

What counts as an asset in a divorce?

In Australia, assets in a divorce can include anything of financial value owned by either person, whether held jointly, separately, or through another structure. Assets may include:

- The family home and other real estate

- Bank accounts, savings and term deposits

- Shares, managed funds and other investments

- Superannuation interests

- Business assets and company interests

- Vehicles, boats, jewellery, artwork and other valuables

- Trust interests or expected distributions

- Debts, mortgages, loans and credit cards

- Cryptocurrency and other digital assets

- Formal valuations for property, businesses, vehicles or other high-value items

Can you protect assets before marriage or divorce?

Yes, you can take steps to protect assets before marriage, during a relationship or before a divorce begins. A financial or prenuptial agreement before marriage can set out how property, debts and financial resources may be dealt with if the relationship ends, including under sections 90B–90UD of the Family Law Act 1975.

A financial agreement may help by:

- Recording what each person owned before the relationship: This can help clarify separate property, savings, investments, business interests or family wealth.

- Setting rules for how property and debts will be divided if you separate: The agreement can outline what should happen if the marriage or de facto relationship ends.

- Protecting business interests, inheritances or family wealth where appropriate: This may be useful when one person brings complex assets or expected wealth into the relationship.

- Clarifying financial expectations in a marriage or de facto relationship: Each person must get independent legal advice, and the agreement must be carefully prepared to ensure enforceability.

How to protect your assets during separation

During separation, you can protect your assets by keeping clear records, securing important accounts and avoiding rushed financial decisions. You should not hide, sell or transfer assets to keep them out of the property settlement. Instead, focus on lawful steps that protect evidence, reduce risk and keep your financial position clear while you work towards an agreement or court orders.

- 01

Step 1: Document your assets and debts

Make a clear list of your property, bank accounts, superannuation, investments, business interests, loans and credit cards. Keep copies of financial documents, including statements, tax returns, payslips, loan records, insurance policies and valuations.

- 02

Step 2: Secure bank accounts and access

Check who can access joint accounts, redraw facilities, credit cards and online banking. You may need to change passwords, update personal contact details and speak with your bank about account controls.

- 03

Step 3: Pause major financial decisions

Avoid large withdrawals, asset transfers, new loans or selling property without advice. These decisions may be questioned later and could affect your position in the property settlement.

- 04

Step 4: Agree on interim budgets

If possible, agree on short-term arrangements for mortgage payments, bills, school fees, insurance and daily expenses. If agreement is not possible, talk to a lawyer to see whether interim orders may be needed.

- 05

Step 5: Review insurance and asset protection

Check that important assets remain insured, including the family home, vehicles, business assets and valuable items. Keep evidence of payments and make sure policies are not cancelled without your knowledge.

Are family trusts protected in divorce?

A family trust is not automatically protected in divorce. In Australia, a family trust may be treated as property or as a financial resource, depending on how it is controlled and used. The court may look at the trust deed, the trustee, the appointor, past distributions and whether one person has real control over the trust.

Common trust issues include:

- A trust may be exposed if one person controls it: This can happen when one person is the trustee, appointor, or key decision-maker. If they can control when assets are distributed, the trust may be seen as part of their financial position.

- Trust assets may be considered if the trust operates like that person’s own asset: This is sometimes raised where a trust is used as an “alter-ego”. In simple terms, if one person treats the trust like their personal bank account, it may be harder to argue that the trust is separate.

- A beneficiary interest may still matter: Even if the trust assets are not treated as property, expected distributions may still be treated as a financial resource. This can affect the way the broader property settlement is assessed.

- A trust will not protect assets if it was made to defeat an anticipated order: Family law courts can scrutinise transfers made before or during family law proceedings. Moving assets into a trust to avoid a property settlement may create serious legal risk.

Need advice about trusts and asset protection?

If you have a family trust, a testamentary trust, or a complex asset structure, it is worth getting advice before you make decisions during separation. Carew Counsel can help you understand how trusts may be treated in family law and whether your estate planning documents still support your long-term goals.

What happens to jointly owned property?

Jointly owned property is one factor to consider when dividing property and finances after separation. In Australia, the family home, investment property and other joint assets are considered as part of the broader property settlement.

The outcome may depend on each person’s financial and non-financial contributions, future needs, the joint loan position and whether the property is sold, retained or refinanced.

Can gifts or inheritances be protected?

Gifts and inheritances may be treated differently from other assets in a divorce, but they are not automatically excluded. Whether they are quarantined, adjusted for or included in the asset pool depends on the circumstances.

Important factors include:

- When the gift or inheritance was received: A late inheritance or windfall received near the time of separation may be easier to distinguish from the shared asset pool.

- Whether it was mingled with joint property: If inheritance money was used for a jointly owned home, business or shared account, it may be harder to separate.

- What records are available: Clear evidence, such as bank records, estate documents and correspondence, can help show where the money came from and how it was used.

Keep inheritance records separate and easy to trace

If you receive a gift or inheritance before or during separation, keep clear records showing where it came from, where it was deposited and how it was used. Avoid mixing inherited funds with joint accounts until you have received legal advice.

%20copy.webp)

How to protect business assets in divorce

Business assets in divorce need careful review because they may affect both the asset pool and each person’s income. A business valuation can help assess goodwill, assets, debts, drawings and future earning capacity. You may also need to review shareholder or partnership agreements, tax issues, and cash flow needs.

- 01

Step 1: Review the business structure

Check whether the business is owned by one person, a company, a partnership, a trust or another structure.

- 02

Step 2: Gather financial records

Collect tax returns, profit and loss statements, balance sheets, BAS records, loan documents and details of drawings.

- 03

Step 3: Clarify each person’s role

Record who works in the business, who manages it and whether either person receives wages, dividends or distributions.

- 04

Step 4: Arrange a business valuation

A formal valuation may consider goodwill, liabilities, cash flow, market conditions and any shareholder or partnership agreement.

- 05

Step 5: Consider settlement options

One person may keep the business while the other receives other assets, a cash payment or a structured settlement.

Do financial agreements really protect your assets?

A binding financial agreement can help protect your assets if it is valid, fair and properly prepared. It must include full financial disclosure, be signed correctly and involve independent legal advice for each person. It can still be challenged if there are issues such as coercion, duress, poor disclosure or major changes in circumstances.

Legal strategies to safeguard your finances

Legal strategies to shield assets in divorce should focus on transparency, evidence and timely action. If there is a risk that money, property or business assets may be wasted, transferred or hidden, a family lawyer can advise on steps to preserve the asset pool while your property settlement is being resolved.

Common legal strategies include:

- Seeking interim orders: Temporary property orders may help deal with urgent financial issues before a final agreement is reached.

- Requesting financial disclosure: Disclosure timetables can require each person to provide bank statements, tax records, business documents and other financial information.

- Using undertakings: One person may give a formal promise not to sell, transfer or deal with certain assets while negotiations continue.

- Applying for an injunction or asset preservation order: In urgent cases, the court may make orders to help prevent assets from being sold, moved or reduced in value.

- Formalising agreements through consent orders: If you reach an agreement, consent orders can make the arrangement legally binding.

Get advice before making financial decisions

If you are worried about money, property or assets being moved during separation, get advice before you act. Carew Counsel can help you understand your legal options and take practical steps that support a fair outcome.

Common mistakes that risk your assets

Some actions can make a property settlement harder, more expensive or less favourable, especially where there are concerns about financial abuse, pressure or control. If you are worried about divorce asset protection mistakes, it is safer to get advice before moving money, selling property or making informal deals.

When to get legal advice about protecting assets

You should get legal advice about protecting assets as early as possible, especially if separation is likely or complex assets are involved. Early advice can help you understand your rights, avoid mistakes and take lawful steps before property is sold, moved or disputed.

Get advice if:

- You own or control complex structures: This includes trusts, companies, partnerships or business interests.

- There is high conflict or urgent financial risk: This may include threats to sell property, withdraw money or stop paying shared expenses.

- You are unsure what forms part of the asset pool: A lawyer can help identify property, debts, superannuation, financial resources and records that may be relevant.

- You are considering an agreement: Before signing anything, get advice on whether consent orders or a financial agreement is more suitable.

Protect your assets with the right legal advice

With over 40 years of family law expertise, Carew Counsel is recognised as one of the most respected family law firms in Victoria. Our award-winning service is built on a client-first approach, focusing on timely and effective resolutions. Our family lawyers and accredited family law specialists are widely regarded as leaders within their field.

If you are separating, have complex assets or are worried about financial risk, our team can help you decide what to do next. We offer flexible consultation options, including a 90-minute consultation with a lawyer where you will leave with a clear roadmap for moving forward.

Table of contents